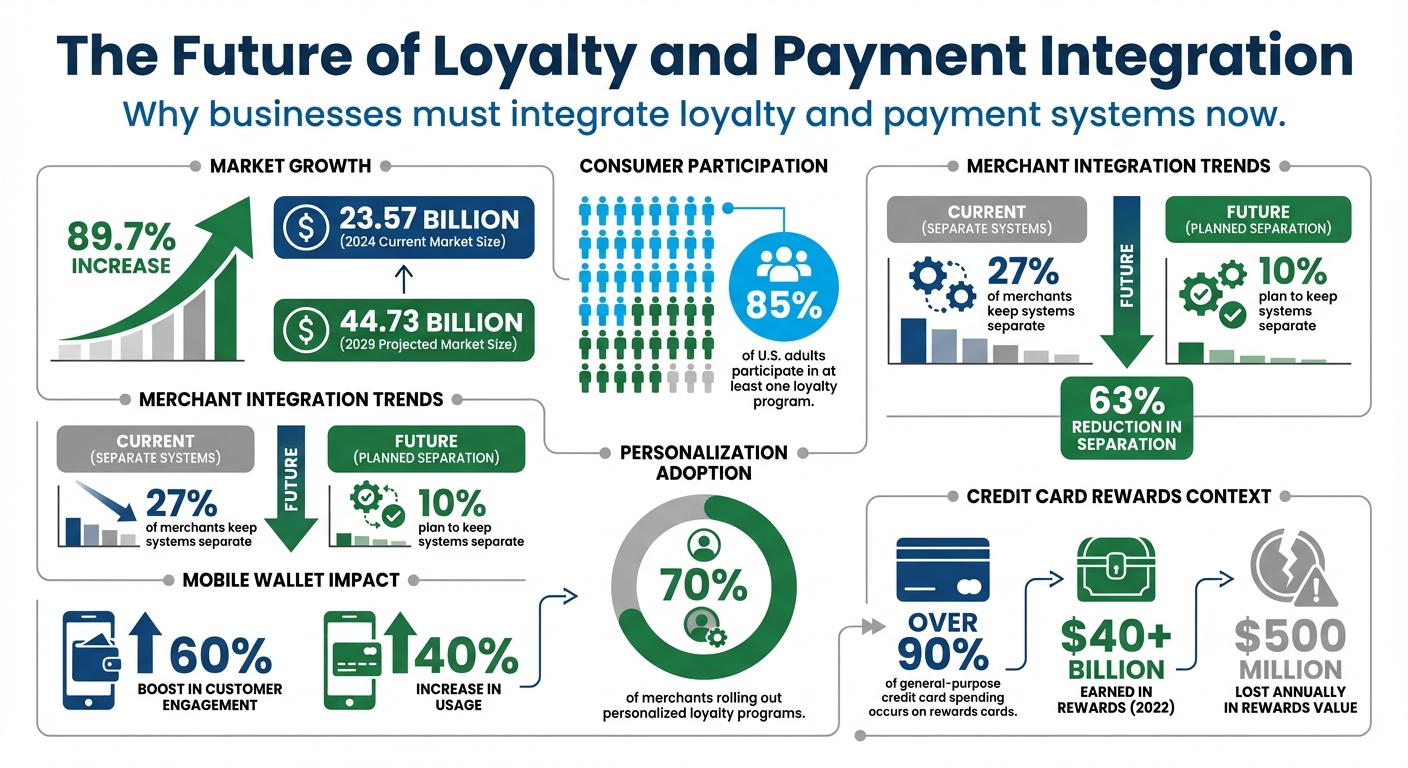

In today’s digital world, people expect loyalty programs and payment systems to work together effortlessly. This shift is reshaping how businesses operate, especially with 85% of U.S. adults participating in at least one loyalty program. Integrating these systems offers faster checkouts, real-time rewards, and better customer experiences. For small businesses, it boosts repeat visits, increases spending, and builds long-term customer relationships. With the loyalty market projected to grow from $23.57 billion in 2024 to $44.73 billion by 2029, acting now is critical for staying competitive.

Key Insights:

- Only 10% of merchants plan to keep loyalty and payment systems separate in the future (down from 27% today).

- Mobile wallet integration can boost customer engagement by 60% and usage by 40%.

- Unified systems reduce delays, improve personalization, and simplify operations.

Challenges & Solutions:

- Disconnected Systems: Legacy setups create inefficiencies. API-based integration and modular systems solve this.

- Fragmented Customer Data: Unified customer identity systems link payment and loyalty profiles seamlessly.

- Real-Time Rewards: Event-driven systems ensure instant updates while preventing fraud.

- Privacy & Compliance: Adhering to U.S. regulations like CCPA and CPA ensures data security and trust.

Loyalty and Payment Integration Statistics: Market Growth and Merchant Adoption Trends

Customer Loyalty Programs Integrating Payment Systems for Success

Challenge 1: Disconnected Technology Systems for Loyalty and Payments

When loyalty and payment systems function independently, businesses often face serious integration headaches. In fact, nearly 47% of organizations report struggling with inadequate system integration. The primary issue lies in businesses relying on a mishmash of technologies that weren’t designed to work together. This lack of cohesion disrupts the seamless experience customers have come to expect – especially in super apps.

Legacy point-of-sale (POS) systems add to the problem by creating data silos. Purchase history might be stored in one system, loyalty points in another, and customer profiles scattered across multiple platforms. This disjointed setup can lead to frustrating scenarios, like customers earning points for an online purchase but being unable to redeem them in-store.

How Separate Systems Delay Real-Time Rewards

Disconnected systems don’t just create inefficiencies – they cause delays. Without real-time communication between payment and loyalty platforms, businesses often rely on batch processing. This means a customer who just made a purchase might not see their updated point balance for hours – or even days.

These delays also make it impossible for staff to provide accurate reward information during checkout. But the problem doesn’t stop there. Traditional loyalty systems are often built as rigid add-ons to POS or e-commerce platforms. This tightly coupled setup means even small updates to a loyalty program can disrupt the entire payment infrastructure. As a result, businesses are often reluctant to experiment with new reward structures, leaving them stuck in outdated systems. These challenges highlight the need for more adaptable and integrated solutions.

Solutions: API-Based Integration and Modular Design

The answer lies in adopting an API-first approach, which treats loyalty as a standalone service rather than an afterthought. Pairing this with a modular, composable architecture allows businesses to break their loyalty systems into independent, specialized components. Each loyalty function – whether it’s issuing points, checking balances, or redeeming rewards – is accessible via APIs, enabling real-time data sharing across payment terminals, mobile apps, and websites.

Instead of relying on one massive, inflexible platform, businesses can use dedicated microservices to handle specific tasks with precision. Take KFC Vietnam, for example. In June 2025, they introduced an API-first loyalty engine to manage tiered discounts and rewards across more than 200 locations. This modular setup let them update loyalty rules without disrupting their payment systems.

Another success story comes from Domino’s, which synchronized its loyalty system with a Customer Data Platform (CDP). This move eliminated manual workflows and data delays, cutting their cost-per-acquisition by 65%. Platforms like meed make this transition easier by offering API-based reward systems that integrate seamlessly with existing payment infrastructures, delivering the real-time performance customers expect – all without the need for extensive custom development.

Comparison Table: Tightly Coupled vs. Loosely Coupled Systems

| Feature | Tightly Coupled (Legacy) Systems | Loosely Coupled (Composable) Systems |

|---|---|---|

| Flexibility | Limited to host platform capabilities | Independent modules can be swapped or updated |

| Integration | Locked into a single vendor or monolith | API-first; works with various CRMs, CDPs, and POS systems |

| Scalability | Difficult; tied to full stack performance | Individual services can scale as needed |

| Risk Management | Small updates can disrupt the entire system | Issues in one module don’t affect overall functionality |

| Time-to-Market | Slower due to complex dependencies | Faster with pre-built connectors and specialized tools |

Challenge 2: Separate Customer Identities Across Systems

When systems fail to communicate, customer identities become fragmented, making it harder to deliver smooth and personalized experiences. For example, a business might use card tokens for payments but rely on email addresses or phone numbers for loyalty programs. This mismatch creates disjointed customer profiles, making it difficult to connect a "payer" with a "shopper." The result? Incomplete transaction histories and missed opportunities for personalization.

This disconnect can cause practical issues too. For instance, in busy environments like grocery stores, asking customers to scan a QR code for loyalty points and then tap their card for payment adds unnecessary friction. Such inefficiencies slow down the checkout process and frustrate both customers and staff.

The Problem of Multiple Customer IDs

At the heart of the issue is the use of multiple, unlinked identifiers. If a customer pays with a credit card but the loyalty system is expecting an email address, the two systems fail to sync. This often leaves loyalty accounts uncredited, especially if customers forget to provide the required identifier at checkout.

Disconnected identities also limit the functionality of loyalty programs. For example, digital wallet passes without proper integration often remain static barcodes (known as "L1" passes). Merchants lose the ability to update balances, adjust tier statuses, or send tailored messages in real time.

The financial and operational costs of bridging these gaps can be steep. Card-linking services, which attempt to unify payment and loyalty systems, often require significant investments – setup fees between $50,000 and $75,000 per payment network (Visa, Mastercard, Amex) and transaction fees ranging from 6 to 10 cents per swipe.

Addressing these challenges requires a centralized approach to customer identity, which we’ll explore next.

Solutions: Unified Customer Identity System for Super Apps

A unified customer identity system can transform how businesses manage customer interactions. By connecting payment methods, digital wallets, and loyalty profiles into a single, comprehensive record, businesses can eliminate the need for separate identifiers. Instead of treating a card alias or an email address as standalone entities, companies can use a back-end system to map all these identifiers to a single "Shopper ID" or reference.

This approach enables payment-linked loyalty, where the payment card itself doubles as the loyalty identifier. For example, when a customer taps their card or phone at checkout, the system instantly recognizes the tokenized card alias and applies the relevant loyalty actions – no extra scans required. This is achieved through a "card acquisition" request that queries the loyalty database before finalizing the payment.

Real-world examples from regions like the Middle East, the UK, and the U.S. show how centralized systems can automatically update loyalty points in real time, without adding steps to the checkout process.

Platforms like meed simplify this integration. Their API-based solutions link loyalty data with payment methods seamlessly, supporting Apple and Google Wallets. This upgrade allows businesses to transition from static "L1" passes to dynamic "L2" passes, which update in real time. Customers can instantly see their updated point balances after a purchase, and merchants can send personalized notifications based on actual transactions.

To make this work, businesses should implement persistent, non-personally identifiable shopper references. These references link all payment methods to a single profile, with new profiles created at checkout only with customer consent.

Comparison Table: Different Identity Strategies for Loyalty Integration

| Identity Strategy | Description | Benefits | Challenges |

|---|---|---|---|

| Card‑Linked Loyalty | Loyalty tied directly to the 16‑digit card number or token | Zero customer effort; works across different POS systems | High transaction fees (6–10¢); setup costs $50,000–$75,000 per network; no real‑time digital engagement |

| App‑Only / QR Codes | Customer scans a code from a dedicated app at POS | High engagement; merchant controls entire ecosystem; enables real‑time offers | High friction; customers may forget to scan; requires app download |

| Unified Shopper Reference | Back‑end ID linking card aliases, emails, and phone numbers | Personalizes experience across online and offline channels; works with multiple payment methods | Requires robust back‑end integration and data privacy compliance |

| NFC/Mobile Wallet | One‑tap payment and loyalty using Apple Pay or Google Pay | Seamless one‑tap experience; automatic enrollment invitations; low friction | Requires VAS‑certified terminals and specific POS software integration |

| L1 Static Passes | Manual entry of card numbers into digital wallet | Easy initial setup for users | No merchant visibility; cannot be updated; static barcode only |

The trend is undeniable: 70% of merchants are expected to roll out personalized loyalty programs soon. To meet these expectations, businesses must unify customer identities. By integrating payment and loyalty systems, they can deliver the seamless and customized experiences that customers now demand from modern super apps.

sbb-itb-94e1183

Challenge 3: Real-Time Loyalty Rewards and Fraud Prevention

Real-time updates are a must for super apps aiming to meet customer expectations. Imagine a customer tapping their card or phone at checkout – they expect their loyalty rewards or discounts to be applied instantly. Any delay, especially in busy spots like coffee shops or grocery stores, can lead to frustration and longer wait times.

Technical Challenges of Instant Reward Systems

Building real-time loyalty systems isn’t as simple as it sounds. Latency is a major hurdle. Every API call adds milliseconds to the process, and if the loyalty engine doesn’t respond fast enough, the payment terminal might time out. This could leave customers without their rewards, creating an unpleasant experience. The situation becomes even trickier with edge cases like partial transactions. For instance, if someone redeems a free coffee reward, the system must apply the discount before calculating the remaining balance.

Keeping data consistent across various channels – whether online, in-store, or on mobile – is another key challenge. Network disruptions or syncing issues can cause mismatched balances, depending on which channel is being checked. Plus, every integration point between the POS, e-commerce platform, CRM, and loyalty engine is a potential weak spot.

Security is another layer to consider. Loyalty accounts are vulnerable to fraud, including account takeovers, fake sign-ups, and data breaches. A real-time system must block suspicious activity before rewards are misused, all while ensuring legitimate customers don’t face unnecessary friction. These challenges call for agile and efficient system architectures.

Solutions: Real-Time Event Systems and Business Rules

To tackle these challenges, businesses should embrace real-time event systems and enforce strict business rules. Event-driven architectures, using webhooks and message queues, can hold rewards during transactions and finalize them only after payment is confirmed. This ensures accuracy, even for partially completed or reversed transactions.

Idempotent processing is another must-have. It prevents rewards from being applied multiple times if an API call is retried after a timeout. Middleware can simplify things by managing data transformations, retries, and communication between the POS and cloud loyalty systems. This reduces the load on front-end systems and improves reliability.

Security measures should be multi-layered. Tokenization and two-factor authentication (2FA) can safeguard loyalty accounts without making things too complicated for users. Real-time fraud monitoring systems are key – they can flag unusual patterns, like multiple high-value redemptions in a short time, and block them before the transaction is finalized.

"Real-time fraud detection systems can also monitor unusual activity and flag potential threats before they escalate into fraud or chargebacks." – Chargeback Gurus

Platforms such as meed offer instant validation and reward updates through API-based integrations. By connecting with Apple and Google Wallets, meed allows businesses to provide real-time updates that customers can see immediately after their purchase, all while maintaining the security needed to prevent fraud.

Comparison Table: Real-Time vs. Batch Loyalty Processing

| Feature | Real-Time (Synchronous) | Batch (Asynchronous) |

|---|---|---|

| Customer Experience | Instant reward redemption and live balance updates for seamless checkout | Rewards updated hours or days later; no instant redemption |

| Technical Complexity | Requires low-latency APIs and real-time database queries | Relies on post-transaction webhooks or file processing |

| Fraud Prevention | Blocks suspicious redemptions before transaction completion | Fraud often detected after rewards are issued |

| Data Accuracy | Validates eligibility during the transaction | Risk of over-redemption due to outdated data |

| Checkout Speed | Combines payment and loyalty in one quick step | May require separate loyalty card scanning |

| System Performance | Demands robust infrastructure for peak transaction volumes | Minimal impact on immediate checkout speeds |

The trend is clear: only 10% of merchants plan to keep payments and loyalty programs separate in the future, a sharp drop from 27% today. As customers increasingly expect instant, hassle-free experiences, businesses must upgrade their systems to deliver real-time rewards while keeping security and performance intact. These investments are critical for creating the seamless, unified experience that’s becoming the hallmark of modern super apps.

Challenge 4: Privacy, Security, and U.S. Regulations

Once technical integration and customer identity challenges are addressed, the next big hurdle for loyalty programs integrated with payment systems in the U.S. is ensuring compliance with strict privacy and security regulations. These systems deal with sensitive data – everything from purchase histories to geolocation – and are subject to heavy regulatory scrutiny. Agencies like the Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC) have made it clear that loyalty programs must meet compliance standards. For context, by 2019, over 90% of general-purpose credit card spending in the U.S. occurred on rewards cards, making these programs a key focus for enforcement efforts. This regulatory landscape sets the stage for the technical and operational solutions that follow.

U.S. Regulations That Impact Loyalty and Payment Integration

Key U.S. privacy laws, such as the California Consumer Privacy Act (CCPA/CPRA) and the Colorado Privacy Act (CPA), impose specific requirements on loyalty programs. For example, under California law, loyalty programs are classified as "financial incentives", requiring businesses to obtain opt-in consent and disclose the estimated value of customer data collected. Meanwhile, Colorado’s CPA governs "Bona Fide Loyalty Programs", mandating that any data collected must be strictly necessary for the program to function.

The CFPB also monitors credit card rewards programs under Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) standards. Businesses risk enforcement actions if they devalue rewards, use hidden terms to revoke points, or experience technical failures during redemption. In 2022 alone, U.S. consumers earned more than $40 billion in rewards from major credit cards – a staggering 50% increase from 2019. However, despite this growth, consumers still lose approximately $500 million in rewards value annually.

"Rewards program operators risk committing unfair or deceptive acts or practices when… rewards that consumers have already earned are devalued; consumers’ receipt of rewards is revoked, cancelled, or prevented based on buried or vague conditions; and rewards points are deducted without consumers receiving the corresponding benefit." – Consumer Financial Protection Bureau

The FTC, on the other hand, enforces "reasonable data security" standards, often targeting loyalty programs in its enforcement actions. Violations can lead to serious financial penalties. For instance, under the CCPA, California can impose civil penalties of up to $7,500 per intentional violation, while Colorado’s CPA allows fines of up to $20,000 per violation.

| Feature | California (CCPA/CPRA) | Colorado (CPA) |

|---|---|---|

| Term Used | Financial Incentive | Bona Fide Loyalty Program |

| Consent | Opt-in consent required | No opt-in; must be voluntary |

| Data Value | Must disclose estimated value of data | Not explicitly required |

| Data Minimization | General requirements | Strictly necessary for the program |

| Cure Period | Eliminated as of Jan 2023 | 60-day period (sunsets Jan 2025) |

Solutions: Privacy-First Design and Secure APIs

Ensuring compliance with U.S. privacy and security regulations requires a focus on privacy-first design and secure API integrations. One essential step is to collect only the data that’s absolutely necessary. For example, if geolocation data isn’t crucial for a reward, don’t collect it – especially since geolocation is often classified as sensitive data that requires explicit consent. This aligns with Colorado’s CPA, which mandates data minimization as a legal requirement.

API security also plays a critical role. Connections between payment and loyalty systems must be encrypted and protected with multi-factor authentication. Financial institutions can even be held accountable for UDAAP violations caused by technical failures on a merchant partner’s system. To mitigate this, businesses should implement robust error handling, conduct regular audits of third-party integrations, and provide consumers with straightforward options to access, delete, or transfer their data.

Avoiding dark patterns is equally important. The opt-out process should be as simple as opting in, and details about redemption values and expiration terms must be clearly displayed – not buried in fine print. Using vague terms like "gaming" or "abuse" to justify the revocation of rewards can lead to enforcement actions.

meed’s secure API integrations address these challenges by emphasizing data minimization and clear consent protocols. Its integration with Apple and Google Wallets ensures customer data is protected throughout transactions, reducing the risk of breaches while delivering fast, real-time reward updates. This approach not only meets regulatory standards but also builds trust with users.

Conclusion: Building a Modern Loyalty and Payment System

Bringing loyalty and payment systems together has become a must for today’s super apps. However, several hurdles stand in the way: outdated technology, scattered customer identities, slow reward processes, and strict U.S. privacy regulations. Thankfully, the solutions are clear. By using API-based integrations, systems can connect more efficiently. A unified customer identity approach eliminates the need for multiple logins and physical cards. Real-time reward processing satisfies customers’ growing demand for instant gratification, while privacy-first designs ensure sensitive data remains secure and compliant with U.S. laws.

The data highlights the urgency of this shift. Right now, only 10% of merchants plan to keep their loyalty and payment systems separate in the future, a sharp drop from 27% today. Additionally, nearly 70% of merchants are gearing up to implement personalized loyalty programs soon. Small businesses that act now will be better equipped to win customer loyalty, boost transaction frequency, and grow without running into tech-related obstacles. Tackling these challenges step by step not only simplifies operations but also strengthens customer relationships.

Steps to Implement Loyalty and Payment Integration

Making this transformation requires a phased approach. Here’s how to get started:

- Phase 1: Set up your loyalty backend. Define clear rules for earning rewards – whether they’re tied to spending amounts or specific purchases.

- Phase 2: Integrate your loyalty program with digital wallets like Apple Wallet or Google Wallet. Use REST APIs or mobile SDKs to allow customers to store loyalty cards on their phones, eliminating the need for a separate app.

- Phase 3: Streamline enrollment with pre-filled forms that pull customer data directly from their digital wallets. This reduces friction and speeds up sign-ups.

- Phase 4: Engage customers with push notifications. Alert them about their points balances, expiring rewards, or location-based offers when they’re near your store. For in-store experiences, ensure your payment terminals support Value Added Services (VAS) for NFC-enabled one-tap payments and loyalty check-ins.

| Implementation Phase | Key Actions | Expected Outcome |

|---|---|---|

| Phase 1: Setup | Define accrual rules and reward tiers | Clear program structure |

| Phase 2: Integration | Connect loyalty systems to digital wallets via APIs | Seamless customer experience |

| Phase 3: Enrollment | Use pre-filled forms for sign-ups | Easier and faster enrollment |

| Phase 4: Engagement | Send push notifications and enable NFC loyalty check-ins | Increased retention and repeat visits |

How meed Can Help

This is where meed comes in. It offers a universal loyalty platform that makes integration simple and effective. With an API-based design, meed connects effortlessly with payment systems and works seamlessly with Apple Wallet and Google Wallet. Customers can access loyalty cards digitally – no need for physical cards or extra apps.

For small businesses, meed is a game-changer. It provides features like digital stamp cards, QR code rewards, and real-time analytics, all without hefty setup costs. Their pricing is straightforward: a free Starter plan for beginners and a Pro plan at $490 per year, which supports up to five locations and 30 active campaigns. Plus, meed’s focus on data minimization and secure APIs ensures compliance with U.S. privacy laws while fostering customer trust.

Whether you’re running a neighborhood coffee shop or managing multiple retail outlets, meed delivers the tools you need to provide secure, scalable, and user-friendly loyalty and payment solutions. It’s a smart way to keep customers coming back while staying ahead of the competition.

FAQs

What are the benefits of integrating loyalty programs with payment systems for small businesses?

Integrating loyalty programs with payment systems takes the hassle out of the checkout process, allowing customers to automatically earn rewards or redeem offers right at the point of sale. No more fumbling with physical cards or entering codes – just the kind of convenience today’s shoppers expect. Plus, this smoother experience can help reduce cart abandonment, keeping more sales on track.

For small businesses, this integration is a game-changer. Returning customers tend to spend 67% more than new ones, so keeping them engaged is key. Beyond boosting spending, integrated systems provide access to valuable transaction data. This data can be used to craft personalized offers, automate marketing campaigns, and test new incentives – all without needing extra software. Tools like meed make it even simpler by offering features like digital stamp cards, QR code rewards, and compatibility with Apple Wallet and Google Wallet. These options let businesses roll out app-free loyalty programs in no time.

By combining payments and loyalty programs, small businesses can streamline daily operations, cut costs, and offer a shopping experience that keeps customers coming back. It’s a practical way to stand out in a competitive market while driving repeat visits and higher sales.

What challenges do businesses face when integrating loyalty programs with payment systems?

Integrating loyalty programs with payment systems comes with its fair share of hurdles. One of the biggest challenges is technical integration. Businesses need a smooth connection between their loyalty platforms and payment systems, which can get tricky, especially when dealing with older or incompatible technologies.

The rise of digital wallets and contactless payments – like Apple Wallet and Google Wallet – adds another layer of difficulty. Many loyalty programs were originally built for traditional card-based systems, making it harder to adapt to these newer payment methods. On top of that, ensuring that points and rewards update in real time during checkout is crucial for a seamless customer experience. This level of synchronization demands a high degree of system coordination.

Another critical factor is security and compliance. Integrating loyalty data with payment systems means businesses must prioritize strong encryption and adhere to strict privacy and payment regulations. Platforms like meed help tackle these challenges by offering straightforward integration with modern payment gateways, real-time balance updates, and compatibility with popular digital wallets. This not only simplifies loyalty management for businesses but also enhances convenience for customers.

How does a unified customer identity enhance the loyalty program experience?

A unified customer identity brings together all the ways a shopper interacts with a business – whether online, in-app, or in-store – into one comprehensive profile. By connecting payment methods, phone numbers, email addresses, or device IDs, businesses can recognize customers effortlessly across different channels. This eliminates the need for repeated sign-ups or manual entries, making the experience smoother. For example, loyalty rewards can be automatically applied at checkout, removing any extra steps for the customer.

With this setup, rewards like points, stamps, or account balances update instantly as soon as a payment is made. Customers can even get real-time notifications about earned rewards or new offers directly on their phones. Thanks to integrations with tools like Apple Wallet and Google Wallet, there’s no need for physical loyalty cards or remembering account details. On top of that, businesses can use this consolidated data to create personalized promotions based on shopping habits, encouraging customers to return and spend more.

meed takes this concept further by offering a universal loyalty platform that simplifies everything. It provides businesses with tools to manage digital stamp cards, QR code rewards, and wallet integrations, all from one dashboard. Shoppers benefit, too – they can view all their memberships in one place, redeem rewards with a single tap, and enjoy a loyalty experience tailored just for them.